The New York Times ran a nice article today by Alan Feaur entitled The Bank Around the Corner. The article does an It's A Wonderful Life-like profile on the Bank of Cattaraugus. Mr. Feaur writes:

“They do things that big banks won’t do,” said Paul Macakanja, the owner of the Jenny Lee diner, which sits on Main Street facing Mr. Cullen’s bank. The diner has no photocopier, and tellers at the bank, he said, will run off copies of his menu, free of charge. “They support you personally,” he added, “because your success is their success.”

The article also discusses how the President of the bank, Patrick Cullen approved an $85,000 loan to an Amish man who only earned $2,400 per year.

“If you know Amish culture, you know his sons work and that everything they earn goes to him until they’re 21 or married,” Mr. Cullen said, observing that the man had eight sons, each earning at least $10 an hour. “So he was fine, but none of that shows up on a credit score.”

There are over 7,000 community banks (assets below $10 billion) in the country and over 7,000 credit unions, yet over 400 community banks have closed in the past three years. BestCashCow data shows that smaller, community based banks tend to offer some of the best rates on deposit and loan products. Community banks also offer more personalized service and as the article illustrates, some of them go to extraordinary lengths to help their community. The Bank of Cattargus is not interested in earning a profit or expanding. As long as President Cullen is able to pay his employees, and his rent, he is happy.

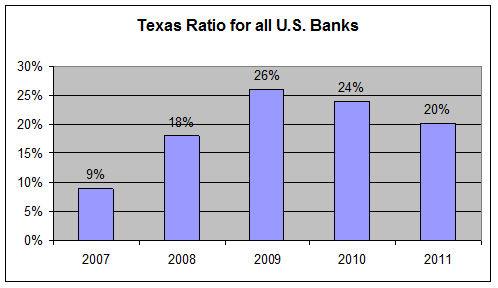

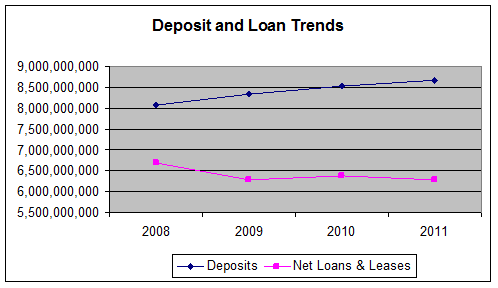

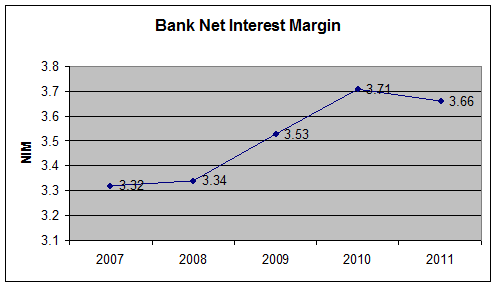

Is this sustainable? From a financial perspective, the bank looks sound. Its Texas Ratio, while rising, is still below the industry norm. The bank has a low return on equity, but it isn't interested in making money. Deposits have grown over the past five years while loans have dipped. So financially, the business model looks stable as long as there is someone to run the bank.

In the wake of the financial crisis and problems at some of the mega-banks, movements have sprung up to convince consumers to go local with their banking. BankTransferDay.org is trying to convince individuals to switch their money from big banks to credit unions. Arianna Huffington's BankTransferDay.org project encourages people to move their money from the big banks to local community institutions. Whether these are long-lasting trends or just a short-term reaction to the financial crisis remains to be seen. The reality is, it's hard to get people to switch banks. The larger banks have grown by gobbling up smaller ones and "assimilating" their customers. While community banks are closing or being acquired every year, new banks are also starting. In fact, the fastest growing banks in the United States are all community banks.

There are drawbacks to community banks. Many don't operate extensive websites or have large ATM networks. Their operations can be slow. I doubt Cattaraugus will be offering mobile banking anytime soon. But for the consumers in their local area, that's probably okay.

Do you bank at a community bank? If so, why? If not, why not? Do community banks have a chance to survive or are mega-banks and Internet banks the wave of the future? Is there room for both? Let us know what you think.

See a map of all banks (large, medium, and community) in your neighborhood.