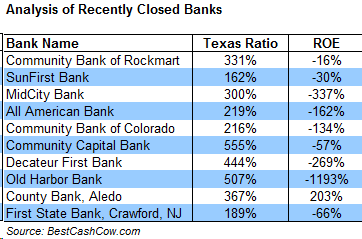

Your local, small community bank may be the growth engine of the banking industry in the future.

BestCashCow analyzed its database to find the fastest growing banks in the United States. We were looking for banks that grew their assets by making loans and provided needed funds to businesses, potential homeowners, non-profits and more. The top 20 fastest growing banks were all community banks that grew at incredible rates right through the financial crisis. It’s not hard to think the sky is falling when listening to financial pundits or reading the mainstream business press. The Euro is collapsing, major banks are in trouble, and the economy is on a road to nowhere. Yet, there are "green sprouts" in the midst of the doom and gloom. So, for some positive news, here are the twenty fastest growing banks since 2006.

The Top 20 Fastest Growing Banks

To determine the fastest growing banks, we analyzed the asset growth of every bank in the United States based on FDIC data from 2006 - 2011. From this data we included only banks that showed four out of five years of positive growth, removing banks that showed huge asset increases in one year and then flat or down subsequent years. This eliminated growth due to accounting changes, or some other non-growth related event.

Who Are the Fastest Growing Banks?

First, unsurprisingly, almost all of the banks on the list are relatively new, small banks. Sixteen of the top twenty were established on or after 2000. Ten of the banks were established in 2006. All of the banks had assets below $1 billion before 2006 although six have grown to be billion plus banks in the subsequent five years. Newly established, small community banks have an advantage when it comes to growth. It is much easier to double and triple $30 million than it is $30 billion. This is true of any new venture or small business. Banks founded in 2006 and after also have another advantage. For the most part, they were able to avoid much of the lending excesses that occurred between 2000 and 2005 and have much cleaner balance sheets. Fourteen of the twenty banks have Texas Ratios below the current national average of 21.06%.

To learn more about these fast-growers, we contacted the number one and number two banks on the list and spoke with Ron Samuels, President of Avenue Bank and Bill Ridenour, the President of John Marshall Bank. Avenue Bank is located in Nashville, TN. Between 2007 and 2011 it grew assets by 2,091% from $26 million to $571 million. In 2011 it had a return on equity of 4.40% and a Texas Ratio of 14.20%.

John Marshall Bank ranked #2 on our list of fastest growing banks. It is headquartered in Falls Church, VA and grew its assets from $23 million in 2006 to $368 million in 2011, a 1,492% increase. It has a 2011 Return on Equity of 6.13% and a Texas Ratio of 2.64%.

Bill Ridenour, the President of John Marshall Bank told BestCashCow that:

"Being relatively new has helped us a great deal… Our advantage is that all the loan growth is based on current market conditions with asset appraisals obtained after the significant downturn in real estate valuations and underwritten in more conservative loan to value and cash flow coverages. The result is a very clean loan portfolio relative to banks that originated a significant amount of their loans at inflated values that are now under water."

In addition, many of these banks are located in areas that avoided the worst of the financial crisis or that are faster growing regions. Four of the twenty banks are located in Texas, two are located in Nebraska. Avenue Bank in Nashville has had a strong regional economy at its back. "The Nashville 14 county area has grown 60% over the last ten years and added 235,000 jobs. Healthcare and education have helped support the local economy, said Mr. Samuels."

Mr. Ridenour from John Marshall Bank also noted that the Washington D.C. metro area "has experienced problems similar to that of the rest of the country but the downturn has been less severe. There are isolated submarkets around the region that have performed better or worse than the average and this is where local market knowledge pays off when underwriting our loan growth."

Experienced Management and Focused Markets

Both Avenue Bank and John Marshall Bank have also grown quickly by having an experienced team that is focused on specific market segments. Avenue Bank has taken advantage of the Nashville market and has strong healthcare and music and entertainment teams. It has a veteran banking team backed by a board of directors that includes Joe Galante, the former Chairman of Sony Music.

John Marshall Bank has much the same. Mr. Ridenour stated "The primary source of our growth has come from the extensive experience that our team of Bankers has in the Washington Metropolitan Area. Most of our management team has over 25 years of banking experience and in some cases over 35 years. This has helped us in two significant ways. First, we have been able to attract a solid team of commercial bankers to our company that bring an extensive network of customer contacts to keep our business pipeline growing. Second, because of our experience, we have a thorough knowledge of our market and focus on the segments that we know best and where we can be the most competitive. That is the small business segment."

Optimistic but Realistic on Economy

In general, both men were optimistic about their regional economies. Mr. Samuels believes Nashville has a bright future and that one "has to be optimistic" and that the "fundamentals are there" for a good 2012. Mr. Ridenour stated that "although we do expect the Washington area to remain one of the strongest banking markets in the country, the budget issues at the national level and their potential impact on the local economy with respect to spending on government contractors does create uncertainty and a need to be cautious."

Community Banks on the Rise?

A clean balance sheet, a decent local market, veteran bankers, defined markets, and a bit of optimism can go a long way in the banking world today. At a time when the mega-banks are reeling and facing increased scrutiny from consumers and regulators, one has to wonder if the time of the community bank has returned. Or, perhaps another way to look at it is which of these smaller banks today might become the larger regional and national banks of tomorrow.

View all community and national banks in your area. BestCashCow provides branch locations, bank rates, bank financial health, and more.