Occasionally, financial planners reach out to me and want to connect on LinkedIn and social media. While I do not hold financial planners in very high esteem since, they are always selling their latest product. I occasionally connect in order to further the reach of BestCashCow.

I do not often engage in debate with these folks, but sometimes I see information shared that is so dangerous to investors and their retirement planning that I need to say something.

That happened this morning with this Wall Street Journal piece: https://blogs.wsj.com/experts/2019/01/06/how-to-play-the-bond-market-during-a-bear-market/

As dangerous as individual bonds may be, they are in principle much less dangerous than owning a bond fund, even a high quality bond fund, since you can always just hold a bond until maturity without having your proceeds drained by a manager in a down environment. At maturity, you get out at par, whereas you may never get out of a bond fund at par.

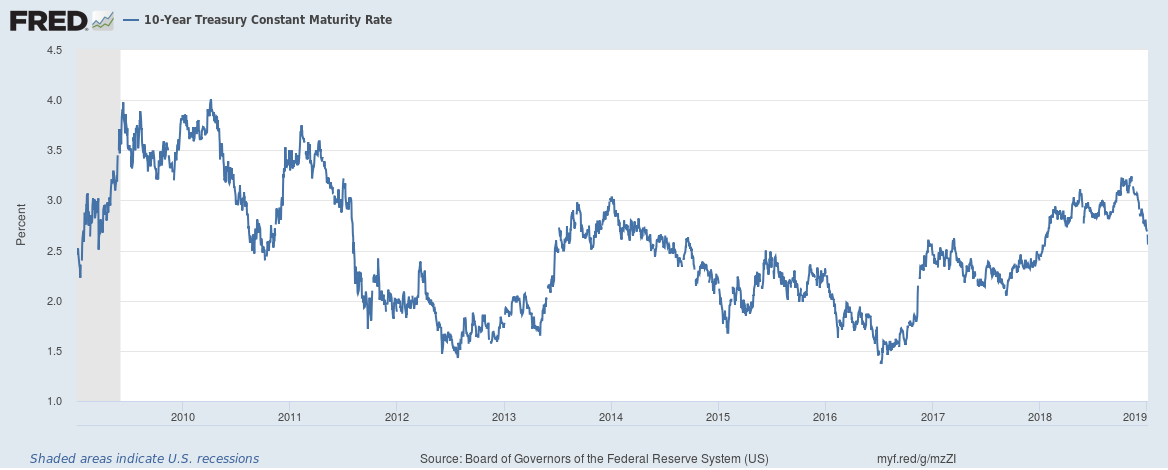

The 10-year US Treasury went to 3.20% last year. As interest rates rose, bond prices fell. Market turmoil over the last 2 months has lead people to seek safe haven in bonds and that has brought US Treasury rates back to 2.60%. But, this is a blip. It is a fleeting moment where you should be selling bonds and bond funds. It isn’t a time to buy. The Federal Reserve is still normalizing interest rates and in that environment the 10-year is still going up.

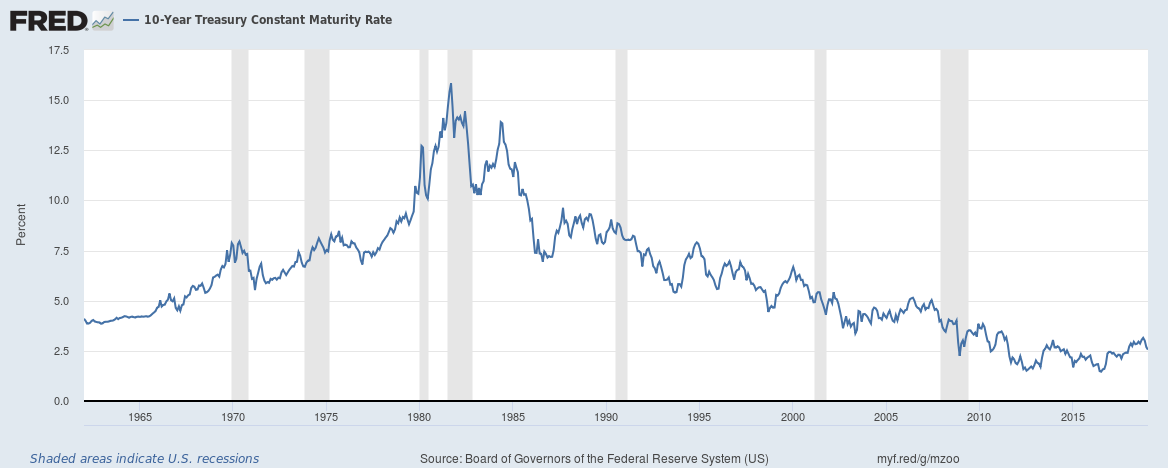

These two graphs from the St. Louis Fed are the best warning I can give. The first, that dates back to 1960, shows how abnormally compressed the 10-year Treasury is by any long-term measure. The second, dating back only 10 years, shows how quickly 10-year US Treasury rates can reverse and rise (even in an environment where interest rates are low).

The “buy bond funds” crowd came out of the woodwork in dramatic fashion in mid-2010 as the 10-year fell from 4.00% to 2.50%. Those who followed this advice saw their funds collapse when interest rates reversed and were in a world of pain in January 2011. While those folks found some opportunities to get out later, opportunities which buyers today may not get.

Stick with savings accounts and short-term CDs for now.

Comments

Allan Roth

January 09, 2019

Ari, here are a few things to consider in which advice is indeed dangerous.

1) I've addressed the myth that bond funds are riskier than bonds many times. People like you and Suze Orman somehow believe that a laddered bond portfolio in a fund has more risk than one owned directly.

https://blogs.wsj.com/totalreturn/2012/07/31/are-individual-bonds-really-better-than-funds/

2) You are in good company thinking you can forecast intermediate and long-term rats with the top economists who have forecasted the direction of interest rates correctly 30% of the time - less than a coin flip.

3) It will probably surprise you that bonds have outpaced global stocks so far this century.

You may want to consider that thinking you know something you don't is more dangerous than using facts and logic.

Is this review helpful? Yes:0 / No: 0

Allan Roth

January 10, 2019

Now that you've hopefully reread the article you found "dangerous" and understand:

1) Bond funds are no riskier than the underlying bonds that could be owned directly.

2) I didn't actually say what you somehow read in to the piece that bonds would outperform anything.

What did you find so dangerous in the piece. High quality bonds such as Treasuries are similar to CDs. Why are they dangerous? I've been a big proponent of CDs for a couple of decades - why are they dangerous?

Is this review helpful? Yes:0 / No: 1

Ari Socolow

January 11, 2019

@Allan Roth Thanks for the comments. You can always hold a CD until maturity and get 100% of your money back with interest (so long as you stay within FDIC limits). You can also always get out of it with a payment of a defined early withdrawal penalty. Presuming a bond does not default, you can always hold a bond to maturity, but the value can go way down (or can go way up) based on interest rate movements before maturity. Bonds, including high quality bonds, therefore represent significantly more risk, especially in a rising rate environment (which is a near certainty with the 10-year at 2.60% and the Fed committed to reducing the size of its balance sheet). A bond fund is still more dangerous than a individual bond (or self-managed portfolio of bonds) because it lacks the a set maturity that an individual bond has. It is managed by a manager who is paid to be invested. When interest rates move dramatically higher, the holder cannot wait until maturity (it never goes back to par), and is guaranteed losses. To invest in these funds and avoid significant losses, you would need to believe that interest rate paradigm has shifted and that the 10-year Treasury will remain at, below or around 2.60% into the indefinite future. And, while you are correct that I cannot forecast the direction of interest rates, a prudent manager also cannot, and would not counsel their clients to take that risk-reward at this point. A CD is infinitely safer and more appropriate than a bond fund at this point in the interest rate cycle.

Is this review helpful? Yes:0 / No: 1

Allan Roth

January 11, 2019

Ari - Thanks but very naive comments:

1) "You can always hold a CD until maturity and get 100% of your money back with interest." If interest rates rise, the opportunity cost of the lower interest you've earned is economically equivalent to the same thing that would happen to a bond or bond fund. If I can't convince you of the absurdity of your argument that a portfolio of bonds in a fund is riskier than owning direct (with less diversification), then I think this ends the discussion as I don't have time to teach you basic economics.

2) "When interest rates move dramatically higher..." Could you send me your track record on predicting the 10-Year T bond rate to see if you are any more accurate than the nations top economists that have forecasted the direction correctly 30% of the time - less than a coin flip. There are those who don't know and those who don't know they don't know.

Of course, CDs with easy early withdrawal penalties give the option of getting out IF rates rise and that's something I've been doing and writing about for nearly 20 years. You could to DepositAccounts.com to see the wonderful actionable information they provide consumers. I have no affiliation with that site.

Is this review helpful? Yes:0 / No: 0

Add your Comment

use your Google account

or use your BestCashCow account