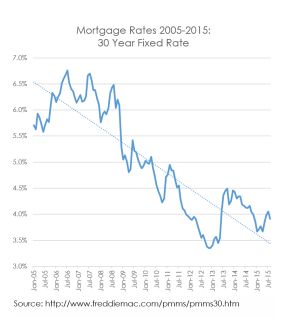

Interest rates remain at historic lows, so for many who haven't refinanced their mortgage recently or have a current mortgage rate above 4.5%, refinancing may be a great financial decision. But how does one determine if now is the right time to refinance?

Interest rates remain at historic lows, so for many who haven't refinanced their mortgage recently or have a current mortgage rate above 4.5%, refinancing may be a great financial decision. But how does one determine if now is the right time to refinance?

The first step is to identify your refinancing goals.

- Do you wish to lower the interest rate on your mortgage or lower your monthly payments?

- Do you wish to combine a first and second note or a primary mortgage and a home equity loan?

- Are you interested in paying off your loan more quickly or building equity in your home more quickly?

- Are you looking to convert some of the equity in your home to cash?

Next is to gather key information about your current mortgage:

- First payment date

- Interest rate

- Beginning loan value

- Current loan value

- Current monthly payment

- Amounts and dates of any additional payments

An important item that may be overlooked in refinancing is that the new loan does come with new closing costs. The closing costs may be paid out of pocket or rolled into the new loan amount. Closing costs for a refinance tend to be higher than for a purchase because you, the borrower, ends up paying for new title insurance. (In many states, it is customary for the seller to pay for title insurance in a purchase transaction.) Some lenders and some title companies will provide a credit or discount to help offset the closing costs.

With your goals identified, your current mortgage information, and a clear expectation on closing costs, you are ready to begin an analysis and make a decision.

You can use online mortgage calculators or amortization tables in a spreadsheet, plus mortgage rates to compare your current loan to a potential refinance. Or, you can talk to me about your goals and receive a customized analysis of your options.

I recently completed a customized refinance analysis for Tom.

Tom's goals are to lower his interest rate and build equity more quickly in his home. He plans to sell his home in 5-10 years and wants to get as much equity as he can on the future sale. Tom had already been paying an extra $100 each month to help with these goals.

I then looked at Tom's credit and current mortgage situation. With excellent credit and current interest rate higher than today's rates, a few scenarios began to emerge for our analysis.

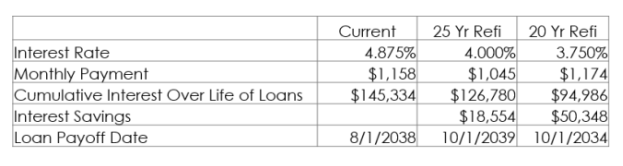

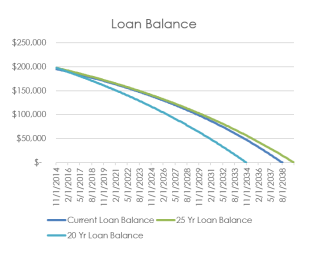

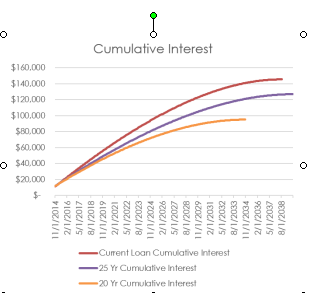

I used a spreadsheet-based amortization table to generate future loan balances, cumulative interest, and pay off dates for three different scenarios: continuation of Tom's current mortgage with the extra payments, a refinance to a 25 Year Fixed Rate mortgage and a refinance to a 20 Year Fixed Rate mortgage.

This analysis indicated that refinancing to a 25 year fixed mortgage may save Tom some interest over the course of the loan, but would not meet his goal of paying off the loan faster. However, refinancing to a 20 year fixed loan would help him pay off the loan nearly 4 years earlier and save $50,000 in interest over the life of the loan. This option clearly met Tom's goals. And if Tom chose to pay extra each month as he had with his current loan, he may save even more in interest, pay off the loan even earlier, and ultimately build more equity more quickly.

This analysis indicated that refinancing to a 25 year fixed mortgage may save Tom some interest over the course of the loan, but would not meet his goal of paying off the loan faster. However, refinancing to a 20 year fixed loan would help him pay off the loan nearly 4 years earlier and save $50,000 in interest over the life of the loan. This option clearly met Tom's goals. And if Tom chose to pay extra each month as he had with his current loan, he may save even more in interest, pay off the loan even earlier, and ultimately build more equity more quickly.

Tom found this analysis to be very helpful in making his decision. We discussed all the ins and outs and ultimately he decided that a refinance would help him achieve his objectives.

Refinancing just to capture a lower interest rate doesn’t always make sense. Be sure to understand your goals and analyze your options.

Interested in refinancing? Follow the steps outlined here or contact a mortgage loan officer for a customized mortgage analysis.

Rebecca Thorburn is a mortgage lending expert with PrimeLending, a national mortgage lender, ranked No. 4 nationally for purchase units.Ms. Thorburn uses her mortgage expertise to deliver mortgage solutions to meet individual home ownership goals. She is also a Certified Divorce Lending Professional®, specializing in helping family law attorneys and in helping those in a divorce situation navigate the options and complicated details related to dividing property, managing current mortgages, and preparing for future mortgages. You can contact her on her website.

Add your Comment

use your Google account

or use your BestCashCow account