The S&P 500 now has a current P/E over 26. Even the most optimistic forecasts that call for all sorts of increased earnings from Trump’s lower taxes and his currency repatriation holidays place the 2018 P/E at 18.

Watching CNBC over the last several days, I have heard a host of explanations for this type of elevated valuation. In addition to the lower taxes and the currency repatriation, they boil down to technology making business more efficient and the “this time is different” type of arguments.

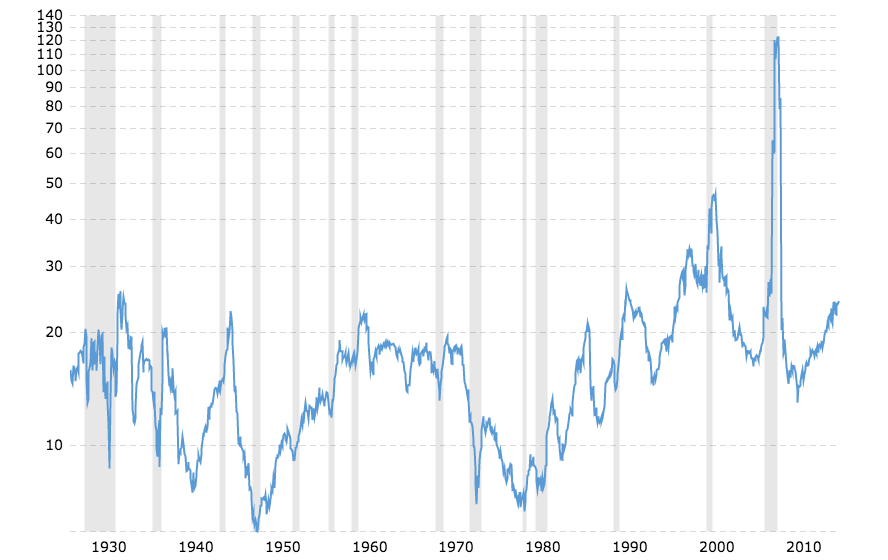

The reality is that this time is no different. The market is trading at a valuation that is, quite simply, unsustainable. As this chart demonstrates, the S&P traded at this valuation twice before – once during the crash in 2000-2001 and once during the crash in 2008-2009 – and on both occasions this valuation was only achieved because earnings fell faster than the market was pulling back.

The S&P did not achieve a 26x multiple in the roaring 1920s. In fact, the market has rarely sustained a current P/E of 18. Its mean P/E over the last century is approximately 15.6 and its median P/E is 14.6. Even if everything goes perfectly under Trump, if the S&P is trading at 2259 in January 2018, it will still be well above its historical averages.

I personally would submit that with a policy that is hostile to free trade, S&P earnings will not be propelled to a level that is much higher than the current level in either 2017 or 2018, and the S&P will revert to trading at its median P/E of about 14 at some point in the next 2 years. My considered predictions, therefore, would imply that the S&P at some point over the next 2 years will fall 40% from its current levels. (If you think that type of valuation is unreasonable to the downside, I would point out that the entire big capitalization pharmaceutical and biotech industries are currently trading at this level.)

There are times when certain stocks can justify P/E ratios well over 26. A company needs to be growing earnings at an extraordinary rate in order to justify these types of valuations.

I am long certain stocks that trade at P/E ratios over 26. I believe that these companies have such strong growth prospects that they justify these types of P/Es. (I am also long stocks that trade at single digit P/E multiples, even though I fear that in a crash, they will also be sold off with everything else).

While certain stocks may justify P/E ratios at the current 26x level, an entire stock market just does not. It may still go higher over the short term, but these valuations for the market as a whole just are not sustainable.

Cash is where you want and need to have a lot of your assets now. See the best savings rates here.

Comments

Dude!

December 09, 2016

Your own chart shows that the the S&P traded at this valuation and sustained it for several years in the late 1990s! It will do it again!

Is this review helpful? Yes:0 / No: 1

Mike Malloy

December 10, 2016

Ari - I think you are correct.

Is this review helpful? Yes:0 / No: 1

JB

December 11, 2016

May take years. Ponzi schemes go on for a while.

Is this review helpful? Yes:0 / No: 1

Add your Comment

use your Google account

or use your BestCashCow account