Let us all get one thing straight, this is an investment-led recovery. Asset prices have rallied strongly from their March 09 lows and corporations have done a phenomenal job of quickly cutting costs and returning to profitability. The casualties reside with the U.S. Government and the U.S. consumer. With an unemployment rate of 10%, housing prices off their highs by more than 30%, and equity markets still 30% away from their highs the average American is feeling the squeeze. Loan delinquencies and defaults are still reaching new highs. The data does not lie:

Click on charts below to enlarge:

Total Delinquencies hit 9.64% of outstanding loans

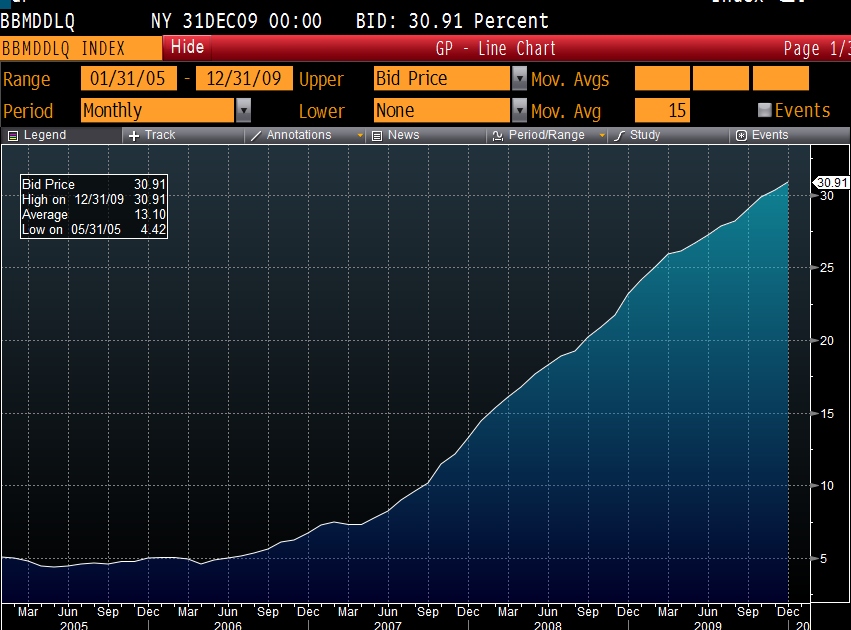

30.91% of all non-agency mortgages are 30+ days delinquent!

11.69% of all non-agency mortgages are in foreclosure!

According to Lender Processing Services 7.2 million mortgages are behind on their payments! In addition to the current foreclosure supply and those people who are debating whether to make strategic defaults on their mortgages because they are upside down, vacancy rates are extremely high and rents are dropping.

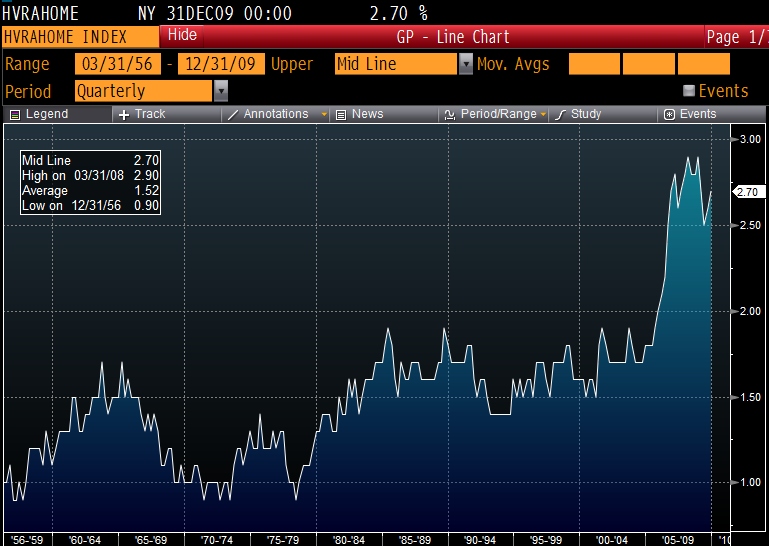

The home Vacancy Rate remains near it high since 1956

Rental Vacancy Rates dwarf past downturns and put extreme pressure on rental rates

So what does continued delinquencies, foreclosures and vacancies mean? It means that housing prices will be near the bottom for a long time to come as inventory is reduced and the unemployment situation slowly gets better. If you are holding onto your house with the hope that the price will rebound, you are holding onto a false dream. The only thing stabilizing factor currently in housing prices is a nice rebate check for first time home buyers and those who take advantage of the upgrade offer. It will be interesting to see what happens this coming summer and fall.

Comments

Sam Cass

February 05, 2010

The other big stabilizing factor is rock bottom mortgage rates. They may go higher although looking at your data I don't see much hope for the economy. Based on that, rates could go lower.

Is this review helpful? Yes:0 / No: 0

Add your Comment

or use your Google account

or use your BestCashCow account