Prosper, a site that connects credit-worthy borrowers with investors today announced that it has raised $17.2 million from several venture capital firms. Prosper has raised $75 million in total.

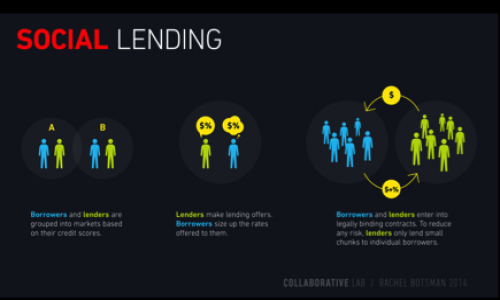

Prosper matches people who need money with people who want to invest it. If you need money, you can list the need, how much you want to borrow, and information about yourself. The company runs a credit check with Experian and then combines that with other information you have provided to create what they call a "Prosper Score." Your listing, along with the Prosper Score appears on the site and investors now have the opportunity to fund your request. I perused the most current listings and the most common uses for money were debt consolidation, home renovation, and auto purchase. In general, lower amounts, below $20,000 seem to be more popular and more successful at soliciting investors.

According to Prosper information, loan rates range between 7.43% for the most credit-worthy borrowers to 36% for the least credit-worthy. Net annualized returns for investors have been 10.4% according to the site. That's not bad, but remember as an investor you can loose your money. In essence, you become a banker when you invest with Prosper and if a loan goes sour, you'll need to write it off. There is no FDIC standing behind you.

Despite the validation from top-tier VCs, social lending is a model that is clearly still evolving. There is vigorous debate on the Internet about Prosper's returns to investors. A negative article written by Mark Gimein: You Are Unlikely to Prosper argues that Prosper's stated returns do not properly include sky high default rates. If these are included, he believes, Prosper is a loser for most investors. He argues that default rates on Prosper loans have been atrocious - as high as 54 percent for loans of 18 percent and up during the three-year payment period. In a Blog responding to this article, Prosper writes that:

"After quoting these cumulative loss results out of context, Mr. Gimein’s bottom line is “After you take defaults into account, investors have lost money on most of their Prosper lending.” Mr. Gimein makes this statement without providing any actual returns data, again leaving the false impression that lenders have lost 39% to 54% on their Prosper lending. The truth is that the median return across all Prosper lenders was negative 3.2%. In addition, 39% of lenders have made money on their Prosper investment. While we would have preferred all of our lenders to have made a profit, a low single digit loss for Prosper lenders in the context of the worst recession since the Great Depression shows great promise for peer-to-peer lending as an alternative asset class for investors. Even a broad index like the S&P 500 saw an annualized loss of 6% in the past three years. Most individual investors have experienced performance substantially worse than this in their investment portfolios and 401k accounts. Something Mr. Gimein fails to discuss."

Prosper also states that since they have put in a new scoring and lending system in July 2009, defaults have dropped significantly with returns above 10%.

Data from Eric's Credit Community validates the fact that Prosper loans are defaulting less. The top chart on the linked page tracks late payments for Prosper loans. The chart shows what percent of loans originagated in that month were late after six months. So for example, ten percent of the loans originated in May 2006 were one or more months late after six months. In June 2010, that number had dropped to around 2 percent. Much of this improvement is because the composition of loans have changed, with less subprime loans and more prime and near prime as shown by the second chart. The rebounding economy may also be helping.

Prosper seems to have been a money loser for investors from its inception in 2006 throughy 2009. In 2009 it changed its scoring models and tightened lending criteria and performance has improved. This improvement was no doubt part of the funding decision made by the VCs. So what does this all mean for you?

Prosper and other social lenders like Lending Club are an evolving model. The social lenders and their investors have a lot of money riding on getting the scoring and system working properly to help investors choose wisely. But even the best tools are subject to the whims of the overall economy. If the economy softens, default rates will go up. You can and you very likely might lose money on Prosper. But you can also make money if you learn the system, invest wisely, and follow the overall economy. In short, you can make money if you think like a banker.

If you decide to give Prosper or other sites like it a shot, consider the following:

1. Do not invest more than you are willing to lose.

2. Get familiar with the site and read some of the supporting Blogs and analysis to understand what you are doing.

3. If you lose money, learn from your mistakes so you do not repeat them.

Add your Comment

use your Google account

or use your BestCashCow account