I have written about several debt-side bank issued Structured notes in the past (an overview of structured notes is provided here). Structured Notes can offer investors much higher yields than savings and CD accounts. Some Notes offer yields higher than bonds from equivalent credits and protect against rising interest rates. Therefore I have suggested that investors allocate money to these instruments as part of a diversified portfolio.

In return for higher yields, investors may have to accept risk depending on the Note. This risks can include:

1) credit risk of the issuer,

2) prepayment or call risk,

3) liquidity risk (there is no secondary market foremost of these instruments),

4) and, kill provisions that could result in interest not being paid for long periods (even the life of the bond).

For these reasons, it is especially important when purchasing a Structured Note that the investor is being offered a return commensurate with the risk, that the risk is reasonable, and that the credit is strong. While Barclays Capital is rated A by S&P, their current offering fails in the other respects.

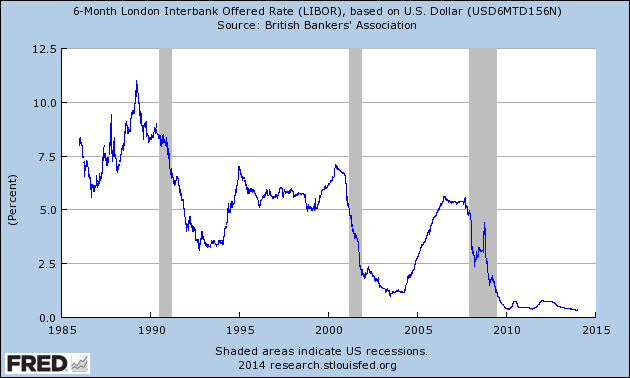

Barclays Capital's current Structured Note offering (CUSIP 06741T4J3) is a 15 year Note which pays 6% in years 1 through 6 and 10% in years 7 through 15. However, if 6 month USD LIBOR trades over 5%, a kill provision in the Note activates, and the Note pays no interest.

As this chart indicates, 6 month LIBOR routinely traded above 5% for the period from 1985 to 2001 and then traded above 5% prior to the 2008 recession.

Barclays is billing the Note as an alternative to a CD that provides a steady stream of income if interest rates fall, or do not rise. It is not a viable CD alternative for two reasons. First, interest rates are rising and in a rising interest rate environment, a 15 year instrument is much more dangerous than a 1 year, 2 year or even 5 year CD. Second, CDs guarantee some return if interest rates do rise and this interest rate does not. In fact, the chart above shows that if we revert to a normalized interest rate environment at any point that this Note is still outstanding and you will likely be earning no interest for a long time.

To boot, this Structured Note is callable by the issuer at any quarterly payment date. Therefore, the Barclays Capital is never taking more than 3 months of interest rate risk, but the purchaser is taking 15 years of interest rate risk. In other words, the purchaser is taking all the risk here and the seller is taking basically none.

I have built a portfolio of Structured Notes for my own account and found many that I like (one that I particularly like was discussed here). This is one that I particularly dislike. It seems that Barclays is going after widows and orphans or at the very least after naïve investors who can no longer remember what a normal interest rate environment is supposed to look like. Others will sleep better by checking out the latest short term CD rates on this site. Caveat emptor!

Comments

Sol

January 11, 2014

Have to agree with you on this one. The call provision is particularly ugly.

Is this review helpful? Yes:0 / No: 0

Add your Comment

use your Google account

or use your BestCashCow account